Updated May 2026

What Is Liability-Only Coverage Insurance?

Liability-only coverage is a policy that includes only bodily injury and property damage liability — the two coverages that pay for harm you cause to others in an at-fault accident. It excludes collision, comprehensive, uninsured motorist, medical payments, and any coverage that repairs your own vehicle or pays your own medical bills. After a DWLS conviction, liability-only is typically the only coverage a non-standard carrier will offer during your SR-22 filing period, and it satisfies state minimum requirements for reinstatement in all 50 states.

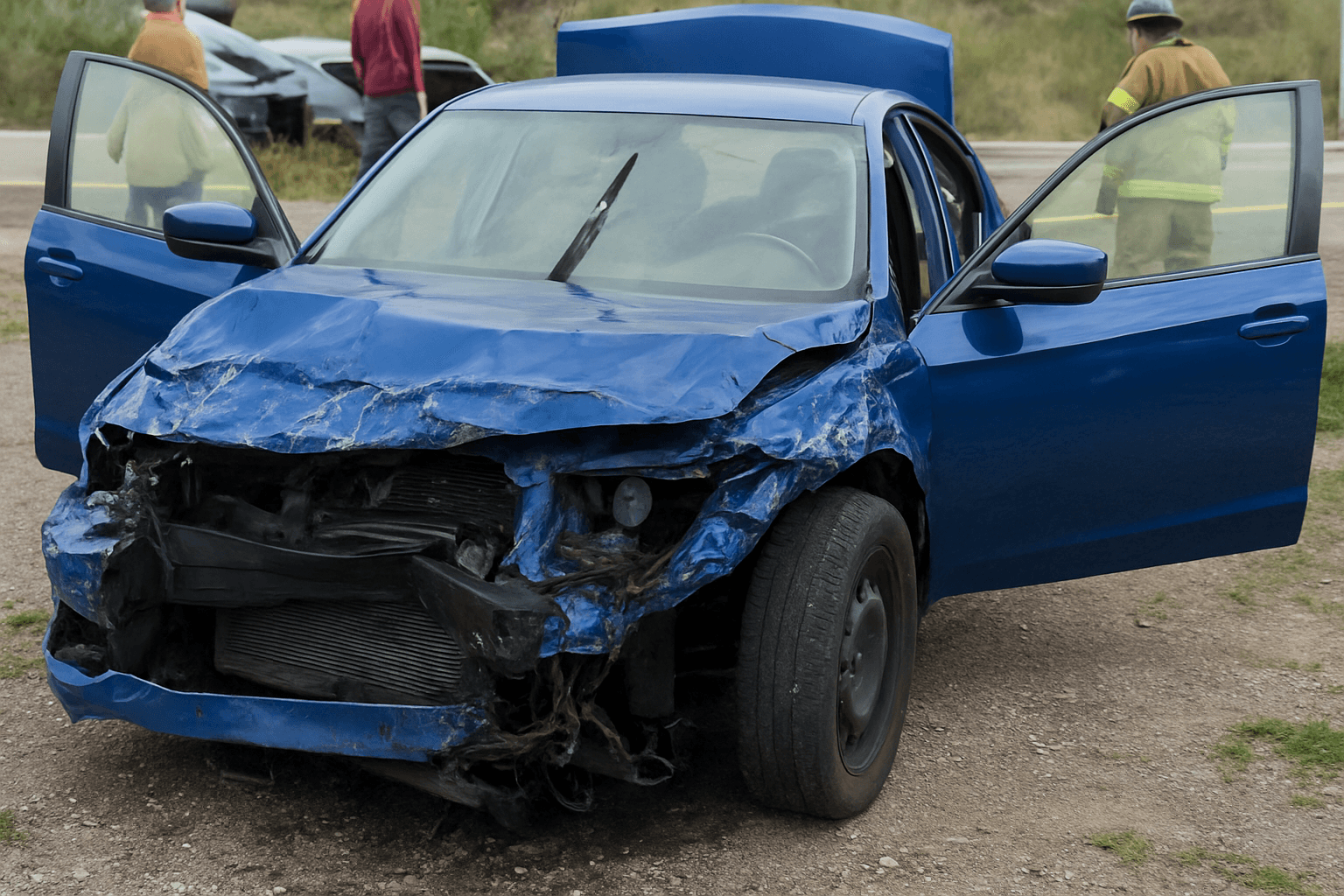

- You're driving to work and rear-end a stopped vehicle at a red light. The other driver has $9,000 in medical bills and their car needs $6,500 in repairs. Your liability coverage pays both bills up to your policy limits. Your own vehicle has $4,200 in front-end damage and you have a broken wrist. Liability coverage pays nothing for your car or your medical bills — you cover those out of pocket or through health insurance if you have it.

- A driver runs a stop sign and T-bones your car, then drives away. Your car is totaled. Liability-only coverage does not pay for hit-and-run damage to your own vehicle. Uninsured motorist property damage coverage would cover this, but that coverage is almost never available to DWLS-convicted drivers during SR-22 filing. You absorb the total loss unless you can identify the other driver and prove fault.

- Your vehicle is stolen overnight and never recovered. Liability-only coverage does not pay for theft. Comprehensive coverage would replace the vehicle minus your deductible, but comprehensive is typically unavailable to drivers with a DWLS conviction until SR-22 filing is complete and at least one year of clean driving is documented. The loss is yours.

How Much Does Liability-Only Coverage Insurance Cost?

Liability-only policies for DWLS-convicted drivers typically cost $120-$240 per month during SR-22 filing, or $1,440-$2,880 annually.

- DWLS conviction severity — misdemeanor first-offense liability premiums run 40-60% lower than felony DWLS or DWLS with an accident involved.

- Original suspension cause — DWLS after DUI generates the highest premiums; DWLS after unpaid fines or FTA generates the lowest in the DWLS category.

- SR-22 filing period length — states requiring 3-5 year SR-22 filing after DWLS see higher premiums than states requiring 1-2 years.

- State minimum liability limits — higher state minimums (e.g. Alaska's 50/100/25) cost more than lower minimums (e.g. California's 15/30/5).

- Driving record beyond DWLS — additional at-fault accidents or moving violations during SR-22 filing can double liability premiums.

- Vehicle type — liability premiums increase for high-performance or luxury vehicles even when only liability coverage is purchased, because at-fault damage potential is higher.

See How Much You Could Save

Get personalized liability-only coverage insurance quotes in minutes.

Who Needs Liability-Only Coverage Insurance?

Liability-only coverage is the required path for any driver reinstating after a DWLS conviction. State DMVs mandate proof of liability insurance at minimum limits before reinstatement is approved, and SR-22 filing requires an active liability policy. If you own a vehicle worth less than $3,000 or you're financing reinstatement costs and cannot afford collision or comprehensive premiums, liability-only is the only realistic option during your SR-22 filing period.

If reinstatement is time-critical for work or family obligations and you own a vehicle, buy liability-only coverage immediately and file SR-22 the same day — delays extend your total suspension period. If your vehicle is worth more than $5,000 and you can wait 6-12 months, some non-standard carriers will add collision coverage after the first year of clean SR-22 filing, reducing your out-of-pocket risk. If you're financing a vehicle, your lender requires collision and comprehensive coverage, which most carriers deny to DWLS-convicted drivers — expect the lender to force-place insurance at 2-3x normal cost or repossess the vehicle.