Your DWLS conviction just triggered carrier non-renewal, and the only insurer willing to write you pulled comprehensive and collision. Here's why comp and collision disappear after DWLS, what liability-only placement means for your vehicle, and how to protect against total loss.

Why Comprehensive and Collision Disappear After DWLS Conviction

Comprehensive and collision coverage require an active, valid driver's license at policy inception and renewal in most states. Your DWLS conviction signals to underwriting systems that you drove while suspended, which creates a licensure gap the carrier cannot ignore. Physical damage coverage (comp and collision) protects the vehicle, but the policy contract assumes the named insured holds a valid license to operate it legally. When you lose that license through DWLS conviction, the carrier's actuarial model flags you as uninsurable for physical damage because the underlying risk—your legal ability to drive—no longer exists.

Most carriers will non-renew your existing full-coverage policy entirely after DWLS conviction. A smaller subset of non-standard carriers will offer you a liability-only policy with SR-22 filing attached, but they strip comprehensive and collision from the quote. This is not punitive pricing—it is underwriting doctrine. The carrier cannot justify paying a total-loss claim on a vehicle driven by someone legally prohibited from operating it. If you file a collision claim while suspended, the carrier will deny the claim and potentially rescind the policy for material misrepresentation.

Liability-only placement after DWLS is the industry's standard response to compound-offense drivers. You are not being singled out. Every driver convicted of DWLS who applies for non-standard coverage receives the same stripped-down offer: liability limits that meet your state's minimum requirements, SR-22 endorsement to satisfy DMV filing, and zero physical damage coverage. The policy exists to keep you legal for reinstatement purposes, not to protect your vehicle.

What Liability-Only Placement Actually Covers After DWLS

Liability-only coverage pays for damage you cause to other people and their property. It does not pay for damage to your own vehicle, regardless of fault. Your state's minimum liability limits—typically 25/50/25 or similar—are the floor. Bodily injury liability covers medical bills, lost wages, and legal defense if you injure someone in an at-fault accident. Property damage liability covers the other driver's vehicle repair or replacement. Uninsured motorist coverage and underinsured motorist coverage are sometimes included in liability-only policies, but not always—check your declarations page.

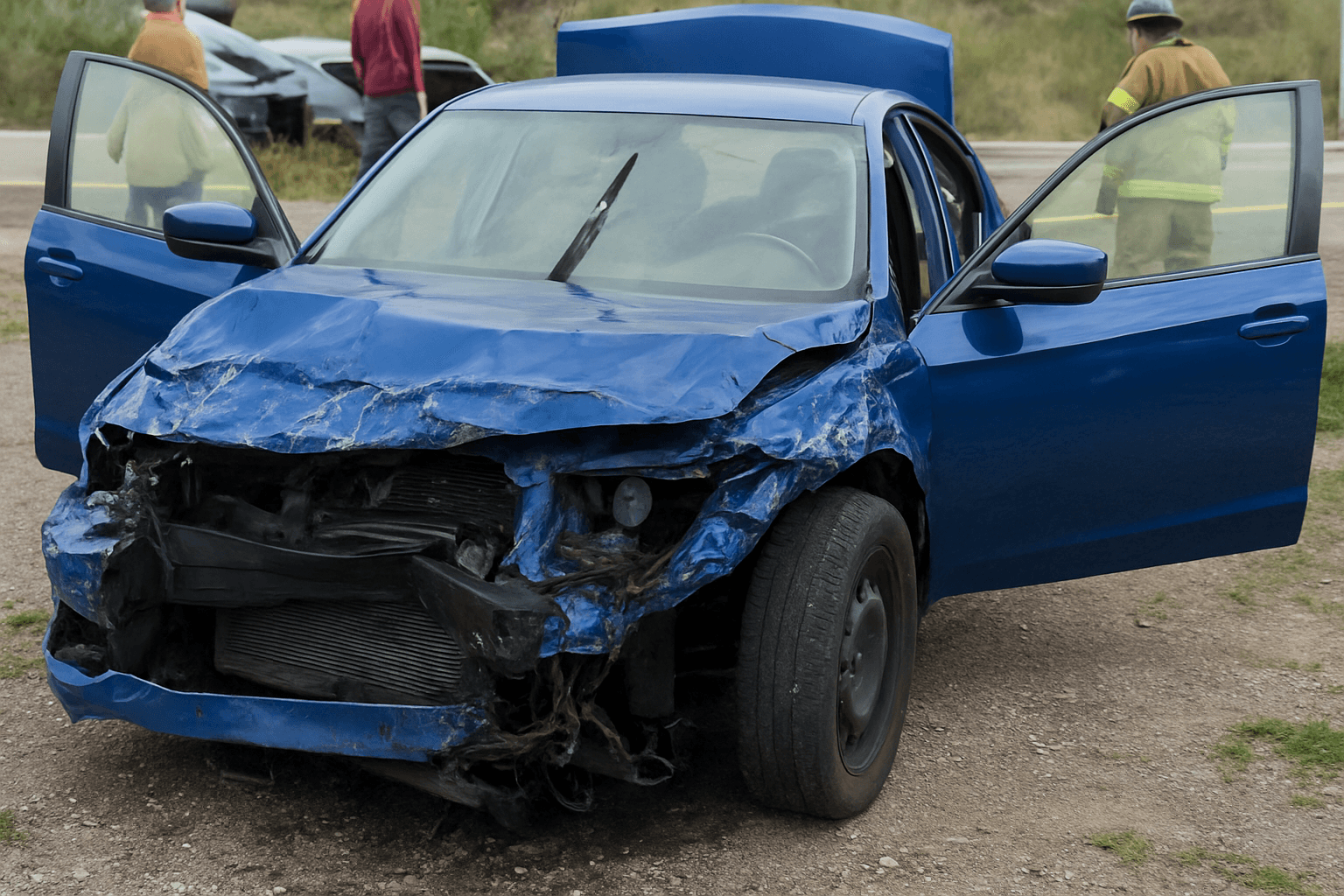

Liability-only placement means you are self-insuring your own vehicle. If your car is totaled in an at-fault accident, you receive nothing from the carrier. If your car is totaled in a not-at-fault accident, you must pursue the other driver's property damage liability coverage directly, which can take months and often settles for less than your vehicle's actual value. If your car is stolen, vandalized, or damaged by weather, you pay the full replacement or repair cost out of pocket. Comprehensive coverage would normally cover theft, vandalism, fire, flood, hail, and animal strikes. Collision coverage would normally cover accident damage regardless of fault. Both are gone.

The SR-22 filing attached to your liability-only policy does not expand coverage—it is a certificate filed with your state DMV proving you carry continuous liability insurance. The filing is required for reinstatement after DWLS in most states, and it remains active for the duration specified by your state, typically two to five years. If you let the policy lapse for any reason, the carrier notifies the DMV within 10 days and your suspension is reinstated immediately. Your vehicle remains unprotected for physical damage the entire time you carry liability-only coverage.

Find out exactly how long SR-22 is required in your state

How to Protect Your Vehicle Without Comprehensive or Collision Coverage

Park your vehicle in a secured location—garage, fenced lot, or well-lit driveway with security camera coverage. Theft and vandalism are the highest-probability total-loss events for vehicles driven by suspended-license holders, and comprehensive coverage is unavailable to you until reinstatement. Remove valuables from the interior, lock doors and windows every time you park, and consider a steering wheel lock or kill switch if your vehicle model is frequently targeted. Comprehensive claims data shows that theft rates for older high-demand models (Honda Civic, Accord, Toyota Camry, Corolla, pickup trucks) are significantly higher in urban areas.

Avoid parking under trees, near flood zones, or in hail-prone areas during storm season. Comprehensive coverage normally handles tree-fall damage, flood damage, and hail damage, but you now carry that financial risk directly. If your vehicle is financed or leased, your lender will receive notice that comp and collision have been removed from the policy. Most lenders require full coverage as a condition of the loan agreement. The lender may force-place coverage at a much higher premium and back-charge you, or they may demand immediate payoff or repossession. Contact your lender immediately after receiving the liability-only policy to discuss options.

Consider selling the vehicle and purchasing a lower-value replacement you can afford to lose. If your car is worth $8,000 and you face three more years of liability-only SR-22 coverage before reinstatement, the cumulative risk of total loss without comp or collision payout is significant. Downgrading to a $2,000-$3,000 replacement vehicle reduces your financial exposure. You still need liability coverage and SR-22 filing regardless of vehicle value, but a total loss on a $2,000 car is easier to absorb than a total loss on a financed $15,000 vehicle.

When Comprehensive and Collision Coverage Becomes Available Again

Comprehensive and collision coverage return to the underwriting table once your license is fully reinstated and you complete the SR-22 filing period specified by your state. Reinstatement means you have satisfied all court requirements from the DWLS conviction, served the additional suspension period stacked on top of your original suspension, paid reinstatement fees, and maintained continuous SR-22 filing without lapse. Most states require two to five years of SR-22 filing after DWLS before the filing requirement drops. Your license must show active, valid status with no restrictions when you apply for full coverage.

Even after reinstatement, expect restricted access to comprehensive and collision for the first 12 to 24 months. Non-standard carriers that wrote your liability-only SR-22 policy will not automatically upgrade you to full coverage at renewal. You must shop the standard market again, and underwriters will see the DWLS conviction on your motor vehicle record for three to five years depending on state reporting rules. Some standard carriers will decline to quote you entirely. Others will offer full coverage but at significantly higher premiums than clean-record drivers pay, with higher deductibles for comp and collision.

Your best path to affordable full coverage post-reinstatement is to maintain a clean driving record for 24 consecutive months after your license is restored. No additional violations, no at-fault accidents, no lapses in coverage. Underwriting models weight recent driving history heavily. A driver with a DWLS conviction five years ago and a clean record since will qualify for better comp and collision rates than a driver with a DWLS conviction two years ago. Time and clean behavior are the only variables that reduce your physical damage premium after DWLS.

Should You Keep the Vehicle or Sell It During Liability-Only Coverage

If your vehicle is financed, contact your lender before making any decisions. Lenders require full coverage—comprehensive and collision—as a condition of the loan. When your carrier strips comp and collision after DWLS conviction, the lender receives automatic notice through the lienholder clause on your policy. Most lenders will send a demand letter requiring proof of full coverage within 10 to 30 days. If you cannot provide it, the lender may force-place coverage at 2 to 4 times your normal premium and add the cost to your loan balance, or they may demand immediate payoff or repossession.

Selling the vehicle and buying a lower-value replacement with cash eliminates lender requirements and reduces your financial exposure during the liability-only period. A $3,000 used vehicle you own outright can be totaled without catastrophic loss. You still need liability coverage and SR-22 filing to satisfy reinstatement requirements, but the absence of comp and collision no longer threatens your transportation or your loan standing. Many drivers convicted of DWLS find this path more practical than carrying a financed vehicle unprotected for three to five years.

If your vehicle is paid off and worth less than $5,000, keeping it may be reasonable if you can park it securely and accept the risk of total loss. Vehicles worth more than $8,000 are harder to justify during extended liability-only coverage. Run the math: if your car is worth $12,000 and you face four more years of liability-only SR-22 before reinstatement, you are self-insuring $12,000 of vehicle value against theft, vandalism, flood, hail, fire, and at-fault collision for 48 months. That cumulative risk often exceeds the transaction cost of selling and downgrading to a cheaper replacement.